Coverage A in Oklahoma: The Dwelling Limit Doctrine

Coverage A is the structural anchor of the homeowners policy. It is not a market value figure and not a real estate metric. It must be determined using Forensic Replacement Cost — the documented cost to reconstruct a home under Oklahoma’s tornado‑driven labor volatility, hail‑driven material turnover, and post‑catastrophe demand surges.

The Oklahoma Rebuild Exposure Tool

This tool quantifies your current rebuild basis against 2026 Oklahoma labor indices. Standard replacement‑cost estimators routinely fail in Oklahoma because they ignore Demand Surge — the immediate spike in labor and material pricing after a regional catastrophe.

Rebuild Exposure Tool

Extended Replacement Cost: The Safety Valve

A fixed Coverage A limit is a liability in Oklahoma. Every homeowner should carry an Extended Replacement Cost endorsement (25% or 50%). When a tornado triggers a regional labor shortage and construction costs spike 20–40% overnight, this endorsement allows Coverage A to expand to the real‑time rebuild cost.

“A tornado doesn’t negotiate. Your policy shouldn’t either.” — Micah Belyeu

The Coverage A Collision Points

Ordinance or Law

Homes built before 2015 often require structural upgrades such as foundation anchoring and high‑wind roof decking. These code‑driven requirements add 15–20% to a rebuild. Coverage A pays for “like kind and quality,” not code upgrades.

Debris Removal

After a total loss, scraping the slab and hauling debris can exceed $20,000. Many policies charge this inside Coverage A, reducing the funds available for reconstruction.

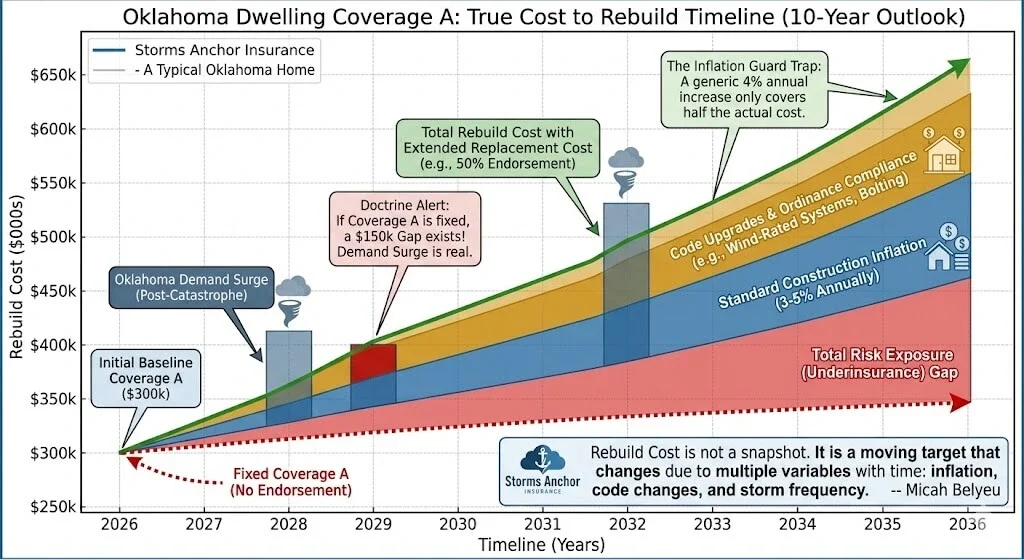

The Inflation Guard Trap

Many carriers apply a generic 4% annual increase. In 2026, Oklahoma construction inflation has exceeded this by 2–3×, leaving many homes 12–18% underinsured.

Many carriers apply a generic 4% annual increase. In 2026, Oklahoma construction inflation has exceeded this by 2–3×, leaving many homes 12–18% underinsured.

Oklahoma Rebuild Variability Matrix

Every Oklahoma rebuild is governed by structural, economic, and environmental variables. This matrix shows how each variable influences the final rebuild cost using Storms Anchor’s doctrine‑locked color system and 2026 Oklahoma cost data.

| Variable | Description | Effect on Rebuild Cost | Magnitude |

|---|---|---|---|

| Cost per Square Foot | Baseline Oklahoma rebuild cost (2026): $191.20/sqft | Direct multiplier of total rebuild cost | Highest Impact |

| Square Footage | Total conditioned living area | Linear increase in rebuild cost | High Impact |

| Demand Surge | Post‑storm labor/material inflation (20–40%) | Applies a percentage increase to all rebuild components | High Impact |

| Roof Complexity | Pitch, facets, dormers, valleys, architectural design | Increases labor hours + waste factor | Moderate–High |

| Foundation Type | Slab, crawlspace, basement | Changes structural and moisture‑control requirements | Moderate |

| Code Upgrades | Decking, bracing, anchoring, energy code, electrical | Adds 10–20% for homes built pre‑2015 | Moderate–High |

| Material Grade | Builder‑grade vs mid‑grade vs premium finishes | Affects cabinetry, flooring, windows, trim, fixtures | Moderate |

| Labor Market Volatility | Oklahoma’s tornado‑driven labor shortages | Raises hourly rates + extends rebuild timeline | High |

| Debris Removal | Scraping slab + hauling debris ($15k–$30k) | Often charged inside Coverage A, reducing rebuild funds | Moderate |

| Supply Chain Delays | Windows, trusses, HVAC, electrical components | Extends timeline → increases labor + rental costs | Moderate |

| Site Conditions | Slope, soil, access, utilities | Affects excavation, grading, and foundation prep | Low–Moderate |

Summary: The three dominant drivers of rebuild variability in Oklahoma are cost per square foot, demand surge, and labor market volatility. These variables compound each other, meaning a tornado‑driven rebuild can exceed the pre‑loss estimate by 20–40% even when reconstructed “like kind and quality.”

The Coverage A Intelligence Suite

A structured set of tools designed to help Oklahoma homeowners test, question, and strengthen their Coverage A decisions before a storm ever hits.

“Coverage A is not a number. It’s a survival threshold.” — Micah Belyeu

Oklahoma Tornado Risk Score Calculator

This calculator uses Storms Anchor’s tornado‑corridor model to score your home’s tornado exposure. Each factor below directly influences the final score and is explained in the results.

“If your Coverage A can’t survive one bad storm, it can’t survive tornado country.” — Micah Belyeu

Demand Surge Simulator

Demand Surge is the rapid increase in labor and material pricing after a tornado or regional catastrophe. This simulator shows how a fixed Coverage A limit behaves when rebuild costs spike. Each variable below includes a Storms Anchor explanation of why it matters.

“Demand surge is the unexpected thief of Coverage A; no one expects there won’t be contractors available to rebuild their home at normal prices.” — Micah Belyeu

Coverage A Collision Map

This map represents how storm paths, neighborhood rebuild costs, and your Coverage A limit can collide.

REBUILD COST: $385,000

GAP: -$85,000

The Forensic Gap: Why the Map Collides

The map above illustrates a $85,000 shortfall—a common sight in the OKC - Moore corridor and the Tulsa Corridor. But where does that money actually go? It isn't just higher wood prices; it’s the Evolution of the Code.

When a "Like Kind and Quality" policy meets a 2026 Building Inspector, a financial collision occurs. The inspector demands 21st-century structural integrity, but your legacy policy only wants to pay for 20th-century materials.

"The biggest check you’ll ever have to write is the one for the upgrades your insurance company said weren't their problem." — Micah Belyeu

Ordinance & Law Cost Builder

Quantifying the "Hidden Invoice" of modern building codes.

- Run analysis to view forensic breakdown.

The Forensic Gap: Quantifying Structural Debt

Think of the Ordinance & Law Cost Builder as a "Forensic Time Machine."

In Oklahoma, building codes aren't static; they evolve every few years to account for what we’ve learned from the last major storm. When you look at your home, you see your sanctuary. When a city inspector looks at your home after a 2026 catastrophe, they see a list of non-compliant structural debts.

Here is the man-to-man breakdown of the forces this tool is actually measuring:

The "Grandfather Clause" Dies at the Slab

Most people believe their home is "grandfathered in" regarding old codes. That is true—until the house is 50% or more destroyed. The moment a tornado crosses that threshold, the "grandfather" protection evaporates. You are now legally required to rebuild to 2026 International Residential Code (IRC) standards. If your policy only pays for "Like Kind and Quality," you are responsible for the price difference out of pocket.

The Three Big "Hidden Invoices”

The tool breaks your exposure into three specific buckets that often blindside homeowners:

Continuous Load Paths: Modern code requires your roof to be physically strapped to the walls, and the walls bolted to the foundation. If you have an older home, you likely have "gravity-fit" construction. Adding these anchors during a rebuild is a massive unbudgeted labor expense.

Roof Decking & Nail Patterns: We now know that standard nailing isn't enough for 130mph+ gusts. Inspectors now mandate specific "enhanced" nailing patterns and thicker decking that your original 1990s or 2005 build didn't have.

Energy & Electrical Mandates: This is the "soft" side of code. Modern energy codes require vastly different insulation, window ratings, and electrical panel safety features (like AFCI breakers) that can add $10,000 to a standard rebuild instantly.

The "Vintage" Vulnerability

The reason the tool asks for your Home Vintage is that the "Gap" is cumulative.

Pre-2000 homes are essentially built to a different structural philosophy. Your "Code Gap" could easily be 25% of your total home value.

2015+ homes were built after Oklahoma began adopting more rigorous high-wind standards, meaning your "Gap" is smaller, but still present due to 2026 energy and electrical updates.

Bottom Line: This builder isn't just playing with numbers; it’s identifying the unfunded mandate sitting inside your walls. If you don't account for this gap now, you're essentially choosing to downsize your home after the storm because you won't be able to afford the "upgrades" required to finish the build.

Would you like to see how these code costs specifically interact with the Demand Surge Simulator above?

EF‑Scale Damage Calculator

Translate meteorological intensity into structural and financial realities.

Forensic Structural Reality

Roof decking lifted. Exterior framing shifts off foundation. Significant water intrusion compromises all interior drywall and flooring. The threshold where Ordinance & Law upgrades are almost certainly triggered upon rebuild.

Policy Type Comparison Engine

Simulating a 2026 Oklahoma Tornado Claim

- Replacement Cost Limited

- Ordinance & Law 10% Included

- Debris Removal Internal to A

- Claim Settlement Actual Cash Value*

*Subject to depreciation

- Extended Replacement 50% Additional

- Ordinance & Law 20% Additional

- Debris Removal Additional 5%

- Claim Settlement Full RCV

Oklahoma Rebuild Cost Index

Forensic Reconstruction Basis (2016–2026 Forecast)

Debris Removal Blind Spot

Calculate how much of your Coverage A is consumed by the slab-scrape.

| Scenario | Typical Cost |

|---|---|

| Standard Slab Scrape | $15,000 - $18,000 |

| Basement Fill/Removal | $25,000 - $35,000 |

| Hazmat/Asbestos (Pre-1980) | $40,000+ |

Explore Home Insurance Topics

These national guides explain how home insurance works across the United States. They remain active until state‑specific pages are built.

Need Help Understanding Your Policy?

If you want help reviewing your home insurance coverage or understanding how your deductible, roof coverage, or exclusions work, you can request a policy review. This is an informational service and does not obligate you to make any changes.

Request a Policy Review

Disclaimer: This page is for educational purposes only and does not determine legal liability, coverage outcomes, claim results, or carrier pricing. Insurance policies are governed solely by the written contract issued by the carrier. All coverage decisions, underwriting actions, premium calculations, and claim determinations are made exclusively by licensed insurance carriers using their own proprietary models and state‑approved guidelines. Policy terms, exclusions, deductibles, conditions, and interpretations vary by carrier, state, and individual risk profile. Nothing on this page modifies, replaces, or supersedes any insurance contract or legally binding document. For specific guidance, refer to your active policy or consult a licensed insurance professional.

© Storms Anchor Insurance. All rights reserved.

Privacy Policy |

Terms of Use |

Licensing & Disclosures